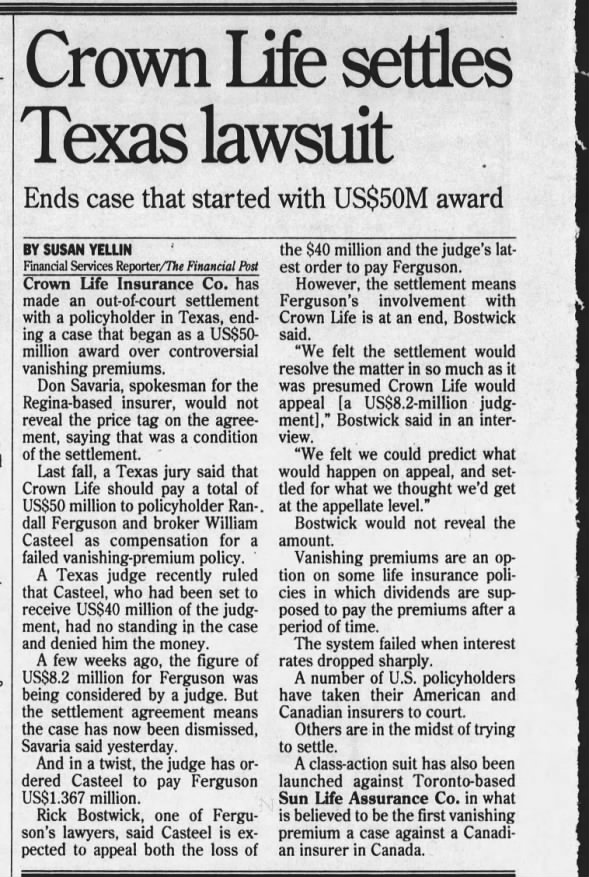

Crown Life v. Casteel - 98-0218

- District Court

- 1991-1995 - Ferguson v. Crown Life and William Casteel

- Indemnity - Love and Bank

- D026 - (p25) - 91-11537 (Ferguson) - COURT'S CHARGE (AND JURY VERDICT) - FILED SEPTEMBER 8, 1995

- TRIAL COURT INFORMATION

- Court Case: 91-11537

- Court: 147th District Court

- County: Travis

- Court: Judge Honorable Joseph Hill Hart

- 1991-1995 - Ferguson v. Crown Life and William Casteel

- Third Court of Appeals

- 03-96-00509-CV

- FROM THE DISTRICT COURT OF TRAVIS COUNTY, 147TH JUDICIAL DISTRICT NO. 91-11537, HONORABLE JOSEPH H. HART, JUDGE PRESIDING

- 1996 - LC - Casteel v. Crown Life - 03-96-00509-CV - Third Court of Appeals

- https://cite.case.law/pdf/11558047/Casteel%20v.%20Crown%20Life%20Insurance%20Co.,%203%20S.W.3d%20582%20(1997).pdf

- Aug. 28, 1997. Publication Ordered July 6, 1999

- search.txcourts.gov/Case.aspx?cn=03-96-00509-CV&coa=coa03

- Supreme Court

- 1998 - LC - Crown v. Casteel - Texas Supreme Court - 98-0218

- 1998 1119 - LC - Crown v Casteel - Texas Supreme Court - 98-0218 - Oral Argument - [AUDIO-link-mp3]

- for petitioner by Mr. G. Alan Waldrop

- for respondent by Cindy Olson Bourland

- Do Agents have the right to Sue?

- 1998 - LC - Crown Life v Casteel - Brief of Amicus Curiae - ACLI - Supreme Court of Texas - 98-0218 - 18p

- 1998 - LC - Crown Life v Casteel - Brief of Amicus Curiae - TALU (Texas Association of Life Underwriters) - Supreme Court of Texas - 98-0218 - 21p

- search.txcourts.gov/Case.aspx?cn=98-0218&coa=cossup

- tsl.access.preservica.com/tda/reference-tools/supremecourtsearch/

- 2002 - LC - IN RE CROWN LIFE INSURANCE COMPANY - search.txcourts.gov/Case.aspx?cn=02-0385&coa=cossup

- CASE: 02-0385

- Date Filed: 04/30/2002

- Case Type: Petition for Writ of Mandamus

- District Court

- 2000 - LC - Crown Life Ins. Co. v. Casteel - 22 SW 3d 378 - Tex: Supreme Court - Google Scholar

- William E. Casteel sold insurance policies as an independent agent of Crown Life Insurance Company.

- One of the policies sold by Casteel led to a lawsuit by policyholders against Casteel and Crown.

- In that lawsuit, Casteel filed a cross-claim against Crown.

- In this appeal from that …

- 2001- LC - Casteel v. Crown Life Insurance

- 2001cv00125 - Texas Western District Court - 02/26/2001 07/11/2001

- Pacer - Yes

- 2000 - LC - Crown Life Ins. Co. v. Casteel - 22 SW 3d 378 - Tex: Supreme Court - Google Scholar

- Broad-form jury charges

- Crown Life exception

- 1995 1201 - AAJ - 'Vanishing premiums' haunt investors, American Association for Justice, by Julie Brienza - [link]

- Ferguson v Crown Life

- 1997 - LR - The Law and Economics of Vanishing Premium Insurance, by Daniel R. Fischel Robert S. Stillman - 37p

- 2000 - LR - Insurance Law, by H. Michelle Caldwell - 43p

- 2004 - LC - DALLAS FIRE INSURANCE COMPANY v. TEXAS CONTRACTORS SURETY AND CASUALTY AGENCY, TOM YOUNG AND FRED THETFORD - 5p

- IN THE SUPREME COURT OF TEXAS

- NO. 04-0215

- ON PETITION FOR REVIEW FROM THE COURT OF APPEALS FOR THE SECOND DISTRICT OF TEXAS

- 5 Respondents contend that in Crown Life Insurance Co. v. Casteel, we extended the reach of article 21.21 beyond claims between an insured and insurer. 22 S.W.3d 378, 385 (Tex. 2000).

- (p4) - But Casteel involved a claim against a life insurance carrier and its agent based on inaccurate language and illustrations contained in life insurance policies sold by Crown’s agent, William Casteel. Id. at 381-82. Thus, Casteel clearly involved the “business of insurance” and not the business of suretyship, which is implicated in this case.

- 2007 - LR - Current Trends in Texas Charge Practice_ Preservation of Error an Crown Casteel - https://commons.stmarytx.edu/cgi/viewcontent.cgi?article=2435&context=thestmaryslawjournal

- 2017 - LC - SKY VIEW AT LAS PALMAS AND ILAN ISRAELY v. ROMAN GERONIMO MARTINEZ MENDEZ AND SAN JACINTO TITLE SERVICES OF RIO GRANDE VALLEY - http://docs.texasappellate.com/scotx/op/17-0140/2018-06-01.green.pdf

- IN THE SUPREME COURT OF TEXAS

- NO. 17-0140

- ON PETITION FOR REVIEW FROM THE COURT OF APPEALS FOR THE THIRTEENTH DISTRICT OF TEXAS

- Argued March 20, 2018 -

- https://www.txcourts.gov/media/1442440/170140cr.pdf

- https://scholar.smu.edu/cgi/viewcontent.cgi?article=1804&context=smulr

- https://www.govinfo.gov/content/pkg/USCOURTS-txsd-4_10-cv-04248/pdf/USCOURTS-txsd-4_10-cv-04248-2.pdf

- https://www.govinfo.gov/content/pkg/USCOURTS-txsd-4_10-cv-01997/pdf/USCOURTS-txsd-4_10-cv-01997-2.pdf

- SHAFFER v. GUARDIAN LIFE INS. CO. OF AMERICAN, (S.D.Tex ... Ferguson, 1997 WL 528822 (Tex. ... the Court bears in mind the Casteel observation that no Texas court has ever found the existence of a fiduciary duty owed ...

- (p54) - Chairman Orrin Hatch (R-UT). Therefore, in any given case, is it true that you do not determine from the outset which party should prevail, whether it be the consumer or some other interest?

- Justice Owen. No, Senator. That would be the complete antithesis of judging.

- Chairman Orrin Hatch (R-UT). Well, I am going to list some cases that undermine any assertion that you invariably rule against a particular type of party and I am going to give you a chance to comment on these, because I found some of those criticisms to be particularly wrong. In fact, all of these have been wrong, the ones who have criticized you.

- Let's take Crown Life Insurance Company v. Casteel.

- William Casteel, an independent agent, sold insurance policies of Crown Life Insurance Company.

- Ruling on a novel issue, you joined the opinion that an insurance agent has standing to sue his insurance company for its deceptive or unfair acts or practices in the business of insurance.

- Am I right on that?

- Justice Owen. That is correct.

2003 0313 - GOV (Senate) - Setting the Record Straight: The Nomination of Justice Priscilla Owen, Orrin G. Hatch (R-UT) - [PDF-273p, VIDEO-CSPAN]

Breazeale v. Casteel, 4 S.W.3d 434

Casetext

https://casetext.com › ... › Ct. App. › 1999 › October

Oct 21, 1999 — Hurren, San Antonio, for William Casteel. Terry Scarborough ... Texas Insurance Code, was remanded to the trial court for additional proceedings.

- 1998 - Casteel v Crown Life

- William E. CASTEEL v. CROWN LIFE INSURANCE COMPANY, Argued November 19, 1998. Decided January 27, 2000 - GoogleScholar

- 1997 - Casteel v. Crown Life Ins. Co. - GoogleScholar

-

- 3 SW 3d 582 - Tex: Court of Appeals, 3rd Dist., 1997 - Google Scholar

- This appeal arises out of a lawsuit involving multiple parties with claims and cross claims concerning the sale of life insurance policies to Randall and Sandra Ferguson.

- Specifically, the issues involved in this appeal pertain to a dispute between appellant William E. Casteel, an insurance agent …

-

- 2000 - LC - Crown Life Ins. Co. v. Casteel - 22 SW 3d 378 - Tex: Supreme Court, 2000 - Google Scholar

- William E. Casteel sold insurance policies as an independent agent of Crown Life Insurance Company.

- One of the policies sold by Casteel led to a lawsuit by policyholders against Casteel and Crown.

- In that lawsuit, Casteel filed a cross-claim against Crown.

- In this appeal from that …

- 2013 - TEXAS CIVIL PROCEDURE TRIAL & APPEAL CASES AND MATERIALS - p1-125 only

- CHAPTER 3. - PREPARATION OF THE JURY CHARGE AND RECEIPT OF THE VERDICT

- Crown Life Insurance Company v. Casteel ............... 206 - <WishList-Book>

- 2014 - Texas Civil Procedure: Trial and Appellate Practice, 2014-2015, By William V. Dorsaneo, III, Elaine A. Carlson, David Crump, Elizabeth G. Thornburg

- https://www.govinfo.gov/content/pkg/CREC-2005-05-18/pdf/CREC-2005-05-18-senate.pdf

- https://www.hicks-thomas.com/recent-news/2016/september/hicks-thomas-llp-gets-50-million-bench-trial-rev/

- A Houston court decided to reverse the decision of a lower court, effectively reversing a land dispute judgment worth $50 million regarding Katy Pin Oak Hospital in Katy, Texas.

- This case may be the first instance of a state appeals court using Crown Life Insurance Co. v. Casteel in a bench trial, a landmark Texas Supreme Court ruling from 2000 that reversed a jury verdict because it was also based on an unsound theory of liability.

- https://www.govinfo.gov/content/pkg/USCOURTS-txnd-3_14-cv-03960/pdf/USCOURTS-txnd-3_14-cv-03960-0.pdf

- 10In their response, plaintiffs cite Crown Life Insurance Co. v. Casteel, 22 S.W.3d 378, 383-84 (Tex. 2000), in which the Supreme Court of Texas held that an insurance agent who

was damaged by an insurance company’s practices that violated § 541.151 had standing to sue the company. But Casteel is factually distinguishable. Setting to one side the fact that plaintiffs are not insurance agents, the plaintiff in Casteel alleged that he had relied on information provided to him by the insurance company about how the policies worked. Casteel, 22 S.W.3d at 381. As the court explains below, in the present case, plaintiffs do not contend that they relied on OraQuest’s alleged misrepresentations.

- 10In their response, plaintiffs cite Crown Life Insurance Co. v. Casteel, 22 S.W.3d 378, 383-84 (Tex. 2000), in which the Supreme Court of Texas held that an insurance agent who

- 2014 - LC - COASTAL AGRICULTURAL SUPPLY, INCORPORATED, v. JP MORGAN CHASE BANK

- Case: 13-20293 Document: 00512705356 Page: 1 Date Filed: 07/21/2014 - 21p

- COURT OF APPEALS - FIFTH CIRCUIT

- Appeal from the United States District Court for the Southern District of Texas

- (p16-) - The Texas Supreme Court has clarified the procedure used where the settlement represents separate and common damages. In Crown Life Insurance Company v. Casteel,65 policyholders sued Crown Life Insurance Company (“Crown Life”) and its independent sales agent, Casteel.66 Casteel cross-claimed against Crown Life.67 With regard to the policyholders’ claims, the jury found that both defendants were liable; that Crown Life had committed the wrongful acts knowingly and bore responsibility for 99% of the policyholders’ damages; and that Casteel had not acted knowingly and bore responsibility for only 1%.68 With regard to Casteel’s claims against Crown Life, the jury found Crown Life responsible and awarded various damages.69 Following trial, Crown Life settled with the policyholders—as part of the settlement agreement, Crown Life was assigned the policyholders’ rights against Casteel.70 The trial court rendered a judgment notwithstanding the verdict as to Casteel’s claims against Crown Life; dismissed the policyholders’ claims against Crown Life because of the settlement; and rendered judgment on the verdict with respect to the policyholders’ claims against Casteel.71 Before the Texas Supreme Court, Crown Life contended that Casteel was ineligible for a settlement credit under the one satisfaction rule.72 Rather, Crown Life argued that when it settled, the jury had already found that Crown Life had acted knowingly, meaning that had the judgment been rendered, the policyholders would have been able to recover additional damages as well as joint and several damages from Crown Life.73 By contrast, the jury had found that Casteel had not acted knowingly, meaning that he was responsible for only the joint and several damages.74 Thus, Crown Life wanted the settlement credit to be applied against the total judgment that would have been rendered—the additional and joint and several damages—rather than the judgment rendered against Casteel.75 The Texas Supreme Court disagreed. “[T]he court should not apply the settlement credit to the judgment that would have been rendered against the settling defendant in determining the credit amount. Instead, the court should look to the judgment to be rendered against the nonsettling defendant and apply established principles governing settlement credits.”76

- The court clarified that a nonsettling defendant can only receive a settlement credit based on the damages for which all tortfeasors are jointly liable, and cannot receive settlement credit for amounts representing punitive damages.77 “[T]he nonsettling defendant is entitled to offset any liability for joint and several damages by the amount of common damages paid by the settling defendant, but not for any amount of separate or punitive damages paid by the settling defendant.”78 The court concluded that Casteel was entitled to a settlement credit as to any settlement amount representing joint damages.79 But once Casteel had offered proof of the settlement amount, Crown Life bore the burden to offer evidence allocating the settlement between joint damages and additional damages.80 In other words, once the nonsettling defendant offers proof of the settlement amount, he is entitled to the settlement credit. Then, the plaintiff must bear the burden to demonstrate allocation of the settlement amount, so that part of that amount represents damages for which the settling and nonsettling defendant are jointly responsible and part of that amount represents damages for which the nonsettling defendant gets no credit.

- Casteel’s lesson is squarely applicable here.